Introduction

BNPL Usage Via Bank Channels Statistics: Buy Now, Pay Later (BNPL) has rapidly grown from a non-mainstream fintech payment option to a credit alternative, driving changes in consumer habits, merchant checkout processes, and banks’ strategic focus worldwide. Initially controlled by fintech innovators like Afterpay, Klarna, and Affirm, BNPL options are now slowly being incorporated into conventional banking networks, blurring the distinction between traditional bank credit and new finance solutions.

In 2025, this trend is not only continuing but also gathering pace, the main factors being customers’ preference for easy payments, the emergence of bank-fintech partnerships, and the upgrading of digital bank infrastructures. However, apart from the gross numbers, BPL usage through bank channels is coming up as a separate sub-segment with its own characteristics, risks, and advantages.

The article examines BNPL Usage via bank channels, bank integration methods, and research-backed insights on BNPL adoption in traditional banking channels for 2026.

Editor’s Choice

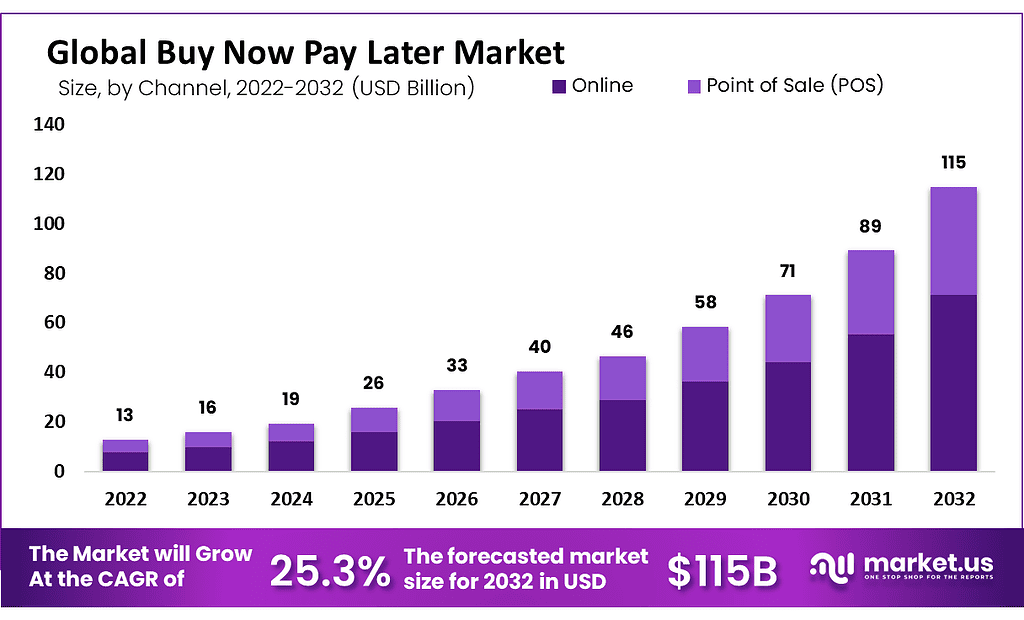

- The worldwide BNPL market is growing at a very fast 25.3% CAGR, rising from US$13 billion in 2022 to an expected US$115 billion by 2032.

- The need for flexible, instalment-based payment options for consumers is the main driver of BNPL’s adoption across digital and in-store commerce.

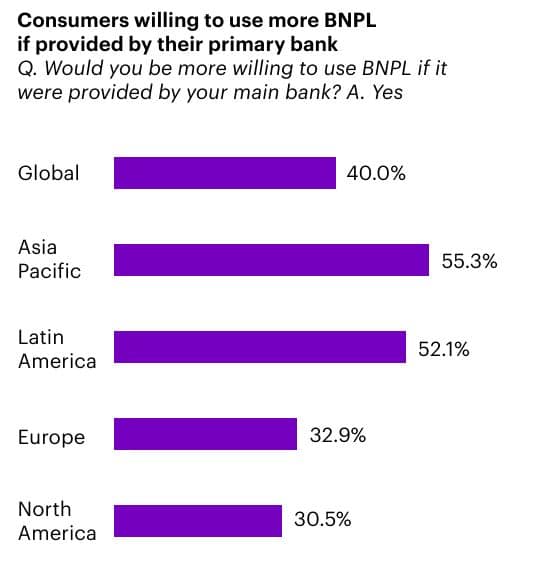

- Trust in banks plays a major role in BNPL adoption, and 40% of global consumers are more likely to go for use BNPL if it is offered by their primary bank.

- Asia Pacific (55.3%) and Latin America (52.1%) have the highest demand for bank-offered BNPL, while North America (30.5%) shows less influence due to its familiarity with fintech.

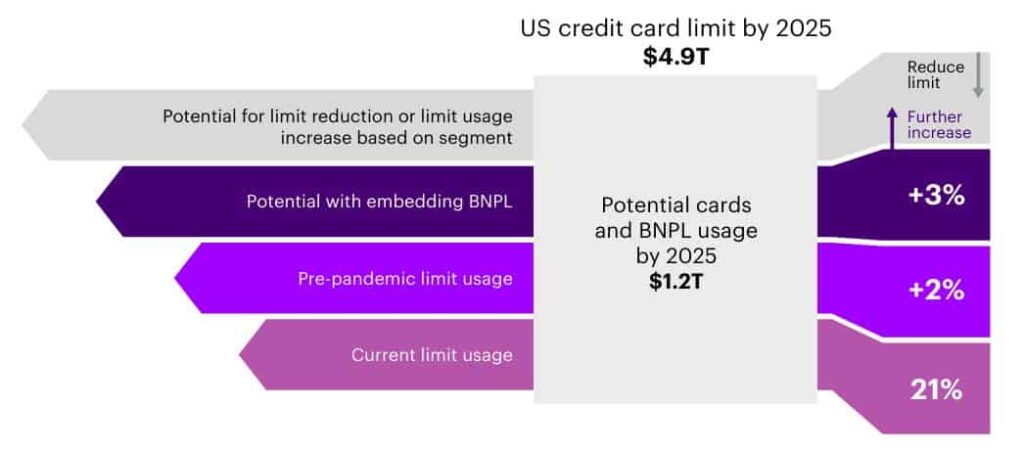

- By integrating BNPL into credit cards, banks would be able to tap into a huge amount of credit that has not been used already, thereby projecting U.S. credit utilization rates to rise from 21% to about 26% by the year 2025.

- Banks in the U.S. with US$3-4 trillion in assets on their balance sheets might generate an additional 10% in revenue by approving BNPL for credit cards. In Europe, large banks could expect income to increase by 6-16%.

- Credit cards with BNPL integration might double the average transaction value and increase the number of transactions by 3x, especially for high credit-risk customers who already have credit lines not fully used.

- The largest share of BNPL transactions is by clothing and fashion (43%), followed by furniture and appliances (31%), personal care (28%), and household essentials (27%).

- More and more consumers are choosing BNPL for everyday spending such as groceries (24%), entertainment (22%), and fitness equipment (15%).

- PayPal is the biggest player in the BNPL market, accounting for 43.08% of payment processing technologies and 68.1% of U.S. consumer adoption in the BNPL sector.

- Klarna has a remarkable position among merchants, enabling BNPL on more than 277,000 U.S. websites and projected to reach 100 million active users by the end of 2025.

- Affirm and Afterpay are both expanding their presence in the market through robust merchant partnerships, with Affirm’s revenue reaching US$783 million in early 2025, a 36% year-on-year increase.

- The use of BNPL is not limited to a specific income group; middle-income consumers opt for it for its flexibility, whereas low-income consumers use it as a necessity.

- The highest percentages of BNPL users are among millennials (33.6%) and Gen Z (26.4%), indicating a close correlation between their payment habits and a digital-first approach.

- Consumers with lower credit scores tend to use BNPL more, with almost 30% of those with a score between 620 and 659 being adopters.

BNPL Usage Via Bank Channels Statistics

- Approximately 78% of surveyed consumers expressed a willingness to use buy now, pay later financing options if they were offered by their existing banks.

- Studies indicate that 70% of current users of these instalment plans would be interested in switching to a version provided directly by their financial institution.

- Around 80% of people who currently use major platforms like Afterpay, Klarna, and PayPal stated they would prefer an instalment product issued through their own bank.

- Over 60% of millennials and 54% of Generation Z consumers are actively interested in utilising bank-issued instalment payment plans.

- Embedding these flexible payment options into existing bank credit cards could increase overall credit utilisation in Europe from 19% to 28%.

- Bank customers with a proven history of using instalment services internally are 30%age points more likely to be approved for a traditional bank loan.

- Consumers who leverage their private instalment payment data through their banks receive loan interest rates that are 1.4 percentage points lower than the market average.

- Nearly 43% of the general consumer population has shown a direct receptiveness to adopting a bank-backed instalment payment product.

- Research shows that 58% of digital banking customers believe these alternative instalment transactions will completely surpass traditional credit card transactions within the next 5 years.

- The integration of these payment plans by United States banks could potentially elevate overall customer credit limits from 856 billion dollars to 1.27 trillion dollars by the year 2025.

Buy Now Pay Later Market Size

- The global market value for these services is projected to grow from USD 16 billion in 2023 to USD 115 billion by 2032, expanding at an annual rate of 25.3%.

- North America led the industry in 2022 by securing a 32% market share and generating approximately USD 4.6 billion in revenue.

- A February 2023 survey highlighted a shift away from physical money, showing that only 9% of Americans pay with cash while 54% rely on debit and credit cards.

- Shopping data from the 2023 Amazon Prime Day sale showed a 20% year-over-year increase in consumers choosing flexible payment plans.

- With current credit card utilization sitting around 21%, integrating these flexible payment options could push U.S. credit limits to roughly USD 1.28 trillion by 2025.

- Financial projections indicate the entire industry could expand by 10 to 15 times its current size by the year 2025.

- In 2022, digital transactions dominated the space, with the online segment accounting for over 62% of the market share.

- Large enterprises captured the majority of the business usage in 2022 by holding a 61% market share.

- The retail industry saw the highest adoption rate in 2022, making up 71.3% of the overall market share.

Consumer Willingness To Use BNPL When Offered By Their Primary Bank

(Source: bankingblog.accenture.com)

- The data we have studied suggests that the use of BNPL products offered by banks could be quite high, but people’s attitudes towards them differ from one region to another.

- On a global scale, 40% of customers said they would be more open to BNPL if it were offered by their primary bank.

- In terms of willingness to adopt BNPL solutions offered by the main bank, Asia Pacific has the highest percentage of consumers who answered positively, at 55.3%.

- Following closely behind is Latin America with the figure of 52.1%, which means that bank-led BNPL could be a very important factor in credit expansion in areas where the traditional credit market is not well-established yet.

- It seems that LATAM consumers prefer to try new financial products when they feel banks are secure and familiar.

- On the other hand, Europe has a moderate reaction with 32.9% of willingness. This could be due to strict credit regulations, mature consumer credit markets, and widespread familiarity with the instalment payment method.

- North America is at the bottom with a figure of 30.5%, indicating that BNPL services offered by fintech companies and retailers have already earned consumers’ trust in that region.

How Embedding BNPL Can Unlock Major Credit Growth Opportunities For Banks

(Source: bankingblog.accenture.com)

- The graphic indicates that U.S. credit card limits will total US$4.9 trillion by 2025. However, only a small share of this capability will be used actively.

- About 21% of credit cards are used in the U.S., indicating that a large share of the available credit is not used. U.S. consumers have, for years, been draining about US$856 billion from US$4.1 trillion in available credit limits, which explains the huge efficiency gap.

- According to the chart, the BNPL-enabled credit cards can push the combined card and BNPL usage to around US$1.2 trillion-1.27 trillion in 2025; hence, the credit utilisation would increase 21% to approximately 26%.

- The rise is driven by two primary factors: encouraging clients to use more of their existing credit limits and allowing the payment of high-priced goods in instalments instead of in one go.

- The picture shows the current usage being further enhanced by an additional 2–3% increase in card utilisation when BNPL is fully embedded and optimised into the card products.

- Customers are more likely to avoid huge one-time charges to their cards and are becoming more comfortable with payments being spread out over time as a result of this growth.

- The revenue opportunity is big from the bank’s viewpoint. By adopting BNPL into its credit card portfolio, a leading U.S. bank with assets of US$3–4 trillion could increase its total card income by approximately 10% in 2025.

- In the same way, a major European bank with more than US$2 trillion in assets could see a 6–16% increase in income from credit cards, depending on adoption rates and customer behaviour.

- Integrating BNPL, in addition to utilisation, could drastically alter spending patterns. Banks might, in fact, be able to increase average transaction (ticket) size by 2x and number of card transactions by 3x, resulting in a steady stream of interchange fees, interest income, and customer engagement that would be almost impossible to interrupt.

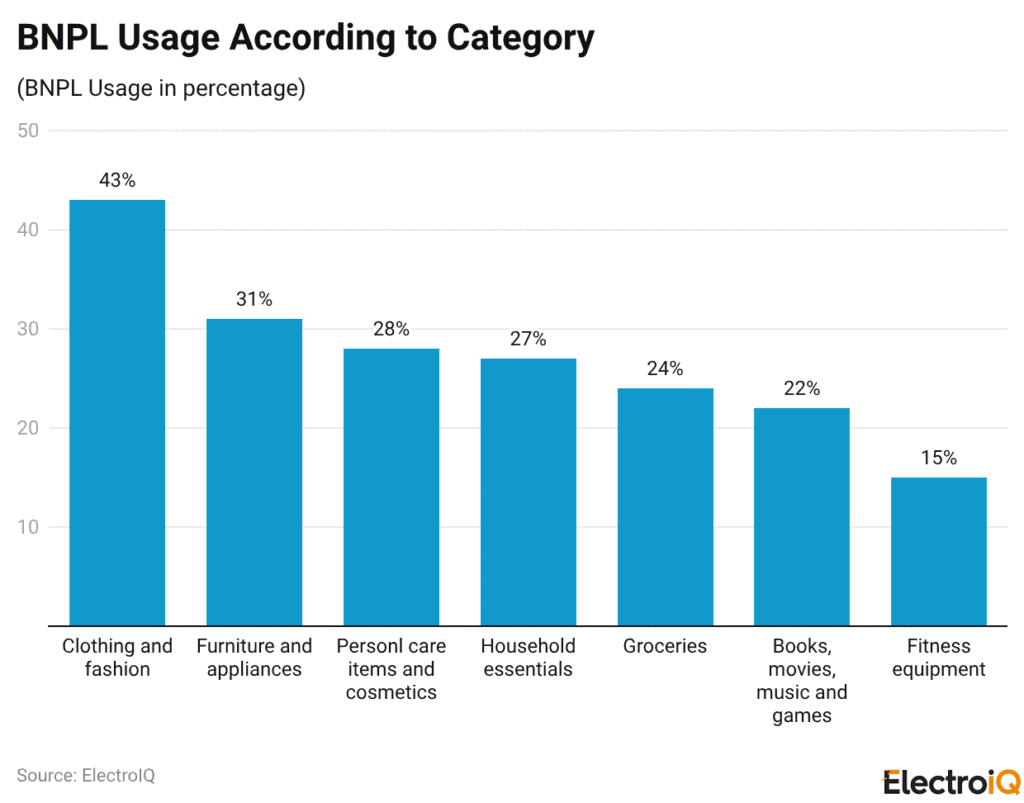

BNPL Usage By Category

(Reference: scoop.market.us)

- Data indicates that Buy Now, Pay Later (BNPL) is a prevalent payment option across both non-essential and essential spending categories, suggesting its growing role in consumer finance on a daily basis.

- The highest penetration is in the clothing and fashion sectors, where 43% of BNPL users opt for instalment plans to finance their purchases.

- Such a situation indicates that buyers are seeking leniency on non-essential but frequently purchased items, especially since fashion purchases often involve several or higher-priced items.

- Following Furniture and appliances comes the 31%, which indicates that BNPL is favoured in larger, more costly household purchases, where consumers might want to do a payment plan rather than pay all at once.

- Personal care and cosmetic products account for 28% of BNPL usage, indicating that people are becoming increasingly accustomed to spreading the cost of basic lifestyle and grooming activities.

- Household items, which 27% of BNPL customers have reported using, are not merely luxury or big-ticket items but everyday necessities, demonstrating the application of BNPL in this area.

- The groceries buying category accounted for 24% of usage, further confirming this trend by indicating the inclusion of BNPL in regular and repeat spending areas and, consequently, supporting short-term cash flow management.

- Books, movies, music, and games as entertainment purchases account for 22% of users, indicating the presence of BNPL in the realm of voluntary leisure spending.

- Lastly, health and fitness equipment, which has been used by 15% of BNPL customers, is also among the items, suggesting that consumers are making the most of the instalment payment option for wellness and health investments.

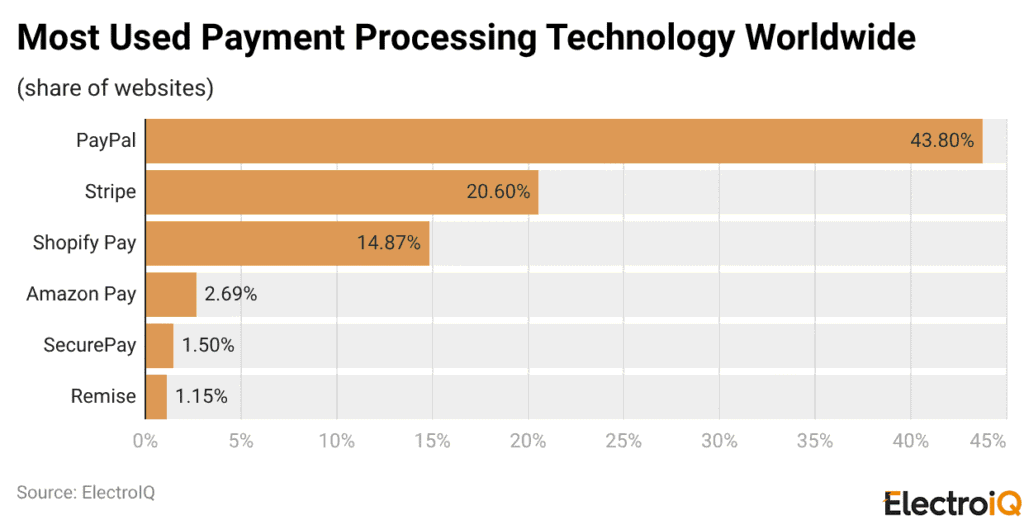

BNPL Industry Growth, By Service Provider

(Reference: digitalsilk.com)

- The information reveals that the fast growth of Buy Now, Pay Later is driven by the consumers’ desire for the major player’s scale and strategy.

- BNPL platforms are increasingly competing on their reach, merchant integration, and ecosystem strength, and these factors directly determine how widely these services are adopted across digital commerce.

- PayPal is the most significant player in the market, with a 43.08% share of the global payment processing technologies market, which includes both traditional payment gateways and BNPL services.

- The strong brand and existing user base drive high consumer adoption of PayPal BNPL, at 68.1% in the U.S.

- The integration of BNPL into a trusted payment platform gives PayPal a significant competitive advantage.

- Klarna is making its mark through widespread merchant and user acceptance. Klarna is the BNPL method available on over 277,000 U.S. websites, underscoring its dominance in the online retail industry.

- Klarna, the world’s largest buy now pay later operator, by the end of Q1 2025, had over 100 million users across the planet, and this was backed up by US$701 million in revenue that the company had at the beginning of the year, which indicated that the company has done very well in terms of monetization alongside rapid user growth.

- Afterpay’s position in the USA is the most powerful, with more than 52,000 online retailers offering BNPL options to their customers. This large number of retailers accepting Afterpay gives the company a dominant role in instalment payments across all retail categories.

- Affirm is another player following the same upward trend, and it is already offering BNPL solutions on more than 18,500 U.S. websites.

- With 21.9 million people using the service in early 2025 and a 36% annual revenue increase to US$783 million, Affirm is a perfect example of how targeting the right partnerships and developing consumer-friendly financing models can lead to both high adoption and profitability.

- Sezzle, while being a smaller player than the top providers, still has a respectable niche that is usually occupied by larger companies, as it accepts payments from more than 22,000 online businesses in the U.S.

- Its persistence in adoption shows that even mid-sized BNPL platforms can be competitive by choosing a specific merchant and customer segment and meeting those segment’s needs.

The Data of Buy Now Pay Later Acceptance Among Different Consumer Groups

- BNPL is not only for financially distressed shoppers but also for consumers who appreciate flexibility and control over their budgets, as well as those who see it as a short-term financial solution.

- Income significantly impacts BNPL use in both directions and through both means. Presumably, about 26.6% of BNPL users earning between US$50,000 and US$100,000 use it as a cash-flow management tool, while the rest use it for different reasons.

- Still, the vast percentage of the latter group, i.e., 26.9%, earns below US$50,000, and this indicates that, for the low-income segment, BNPL is less of a luxury payment choice and more of a tool to overcome low liquidity.

- According to the latest reports, Millennials hold the dominant position as the most significant group of BNPL users in the U.S., with a percentage of 33.6% and then, Gen Z with 26.4% just a step behind them.

- It’s quite clear that the younger crowd is the one most likely to pay in instalments, as evidenced by the popularity of PayPal’s “Pay in 4,” which is used by 51% of customers, split between Millennials and Gen Z.

- This is a clear indication that BNPL has not only adapted to younger generations’ digital preferences and spending habits, but that Gen X remains relevant, as they comprise 35% of Pay in 4 users.

- Cultural and ethnic factors also play a role in determining BNPL use. Black Americans are the largest group of BNPL users, at 25%, followed by Hispanic Americans at 21%.

- These numbers imply that BNPL is a significant source of financial support in communities that might otherwise have difficulty obtaining credit through traditional channels.

- Besides, one out of five shoppers aged 18 to 32 starts their purchasing process at BNPL marketplaces, which indicates that these sites are increasingly being recognized as both product discovery and shopping channels rather than only payment facilitators.

- Gender differences can be observed, but their scope is rather limited. In 2024, 15% of women, compared with 12% of men, adopted BNPL services.

- Around 30% of adults with credit ratings between 620 and 659 used the BNPL service, compared with almost three times that rate among people with scores of more than 720.

- The indicators of financial stress give a clearer picture of why the BNPL behaviour occurs. A majority of users (55%) say they choose BNPL because it allows them to buy items that would otherwise be unaffordable.

- In 2024, 77.7% of BNPL users had to resort to at least one financial coping strategy, such as working extra hours, borrowing money, or using savings, whereas only 66.1% of non-users did so.

- Additionally, 57.9% of BNPL users had experienced a major financial interruption, such as losing a job or incurring unexpected bills, compared with 47.9% for non-users.

- By contrast, the state of being prepared for emergencies reveals a critical vulnerability among BNPL users.

- Just 37% of them could, without any stress, pay the full amount in cash or with a credit card during an emergency, whereas the same percentage among non-users is 53%.

- These findings, combined, suggest that BNPL is located at the intersection of easy and hard, functioning equally as a budgeting tool for the economically stable and a coping mechanism for those experiencing economic uncertainty.

Fintech vs. Traditional Banks Statistics

- Although pure-play fintech companies like Klarna, Affirm, and Afterpay currently control the majority of the global Buy Now, Pay Later (BNPL) landscape with an estimated 57% to 60% market share as of 2025, traditional banks are actively narrowing this gap.

- Traditional bank-issued BNPL products are emerging as the fastest-growing segment in the market, projected to grow at a Compound Annual Growth Rate (CAGR) of 21.19% through 2031, significantly outpacing the broader BNPL industry average.

- A major catalyst for this shift is consumer trust, as a recent PYMNTS and Amount study found that more than 70% of current BNPL users would prefer to use an instalment service offered directly by their primary bank rather than a standalone fintech app.

- This preference is heavily supported by McKinsey data showing that 50% of consumers maintain a high level of trust in large traditional banks to handle their digital payments securely, while standalone fintech apps consistently rank the lowest in consumer trust across all financial provider categories.

- Shoppers are increasingly drawn to bank-led solutions like Chase Pay in 4 or Citi Flex Pay because of the sheer convenience of app consolidation, which allows them to manage their instalment plans directly within their existing banking portal without the friction of downloading a new app or creating a separate account.

- Traditional banks are capitalising on this seamless experience by integrating BNPL functionality directly into existing card networks, with the share of traditional issuers offering card-network instalment plans (such as Visa and Mastercard Instalments) rising to 36% in 2024.

- Regulatory shifts are also heavily tipping the scales in favour of traditional banks, as agencies like the Consumer Financial Protection Bureau (CFPB) enforce stricter affordability assessments and credit reporting rules that banks are already structurally equipped to handle, whereas these same rules drastically increase operating and compliance costs for pure-play fintechs.

Default Rates and Risk Management in Bank-Led BNPL

- Traditional banks operate with a fundamentally lower risk appetite than pure-play fintechs, relying on comprehensive financial underwriting rather than the superficial “soft” credit checks used by standalone Buy Now, Pay Later (BNPL) apps to maximise rapid user acquisition.

- The lenient approval processes used by standalone fintechs have led to a severe surge in late payments, with recent industry data from Prodigal showing that fintech BNPL delinquency rates rose from 34% in 2023 to an alarming 41-42% by 2025.

- This spike in missed payments is heavily driven by the phenomenon of “phantom debt” and loan stacking, as a comprehensive 2025 Consumer Financial Protection Bureau (CFPB) report revealed that 63% of BNPL borrowers actively held multiple simultaneous loans, while 33% juggled debt across several different providers without it appearing on standard credit reports.

- Persistent inflation has severely impacted consumers’ repayment capacity across the board, eroding purchasing power and forcing vulnerable demographics to use BNPL for essential daily expenses, thereby dramatically increasing the likelihood of default when household liquidity dries up.

- To combat these systemic market risks, traditional banks natively integrate BNPL into their ecosystems to leverage massive, pre-existing repositories of customer data, analysing real-time cash flow, direct deposit histories, and broader spending habits to assess a borrower’s true repayment capacity.

- Because banks have direct, panoramic visibility into a consumer’s financial health, they can actively prevent the dangerous credit overextension frequently seen in standalone apps, successfully mitigating risk even though typical BNPL users have a high credit card utilisation rate of 60% to 66%.

- This superior, data-driven risk management strategy not only protects the bank’s balance sheet but also directly benefits the consumer; a 2025 study published by the FDIC demonstrated that banks utilising internal proprietary data for BNPL underwriting were able to offer reliable customers interest rate discounts of roughly 1.4 percentage points compared to the broader market.

The Regulatory Landscape for Bank BNPL in 2026

- The global regulatory environment for Buy Now, Pay Later is undergoing a massive transformation in 2026, transitioning from a lightly monitored alternative payment method to a strictly regulated credit ecosystem.

- In the United Kingdom, the Financial Conduct Authority (FCA) published its finalised rules on February 11, 2026 (Policy Statement PS26/1), mandating that all BNPL providers must be formally authorised and fully comply with the Consumer Duty by the official regulation day of July 15, 2026.

- This UK regulatory shift targets a market that has ballooned from just £0.06 billion in 2017 to over £13 billion, officially bringing approximately 11 million British BNPL users (roughly 20% of UK adults) under formal consumer credit protection.

- Under the new FCA mandates, lenders are legally required to conduct strict, proportionate affordability checks and report lending data to credit reference agencies, a move designed to eliminate the risk of hidden consumer liabilities.

- In the United States, a January 2025 report published by the Consumer Financial Protection Bureau (CFPB) highlighted the severe risks of this hidden liability—often referred to as “phantom debt”—revealing that 63% of BNPL borrowers originated multiple simultaneous loans during a single year.

- The same CFPB report noted that 33% of these borrowers stacked loans across multiple different fintech platforms simultaneously, effectively hiding their true debt-to-income ratios because the majority of these loans were not furnished to the three Nationwide Consumer Reporting Companies.

- Regulators are particularly concerned about this phantom debt because the CFPB found that consumers who actively use BNPL carry significantly higher balances on other unsecured credit, including an average of $871 more in traditional credit card debt and $5,734 more in student loans than non-users.

- This aggressive push by the FCA and the CFPB to mandate credit bureau reporting and strict affordability assessments heavily favors traditional banks over standalone fintech companies.

- Because traditional financial institutions already possess robust, bank-grade compliance infrastructures and have decades of experience complying with strict truth-in-lending laws, they can easily absorb the costs of the new 2026 regulations.

- Traditional banks already actively furnish data to credit bureaus and use automated, comprehensive creditworthiness assessment tools in their daily underwriting, allowing them to instantly meet the new regulatory standards at a fraction of the cost required by tech-first startups.

- Furthermore, as global regulators now mandate clear dispute resolution processes—such as granting UK consumers the right to escalate unresolved BNPL issues to the Financial Ombudsman Service—banks can seamlessly route these disputes through their pre-existing customer service and fraud-resolution departments, avoiding the massive operational overhead that currently threatens the profitability of pure-play BNPL providers.

Conclusion

BNPL Usage via Bank Channels Statistics: Buy Now, Pay Later (BNPL) is a payment option that has been in the market for some time and has become the norm in digital payments. North America and Asia Pacific have been the largest adopters of this service, with the US and Chinese markets alone accounting for a significant share of the global BNPL trend. The global BNPL market size was US$26 billion in 2025 and is expected to grow to over US$100 billion by the decade’s end.

Banks are believed to play an important role in building consumers’ trust in the adoption of BNPL in the future, especially in Asia Pacific and Latin America. By offering BNPL through credit cards, banks can easily reach and sell to a larger customer base, thereby increasing their revenues. The use of BNPL covers both necessities and luxuries, and its acceptance has no barriers of income, age, or credit history, thus making it both a convenient and lifesaving tool.